Global gas markets are no longer reacting to short-term shocks—they are operating within a structurally tight system. What once appeared to be a temporary squeeze has evolved into a more persistent imbalance, where supply growth struggles to match steady, and in many cases rising, demand. Even as prices have cooled from crisis-era peaks, the underlying dynamics remain unchanged: limited supply flexibility, expanding LNG dependence, and a market that reacts quickly to even minor disruptions. This is no longer a cycle—it’s a condition.

Demand Isn’t Backing Off

Natural gas demand continues to defy expectations of decline. Instead of fading under the weight of energy transition policies, consumption has stabilized and, in key regions, strengthened. Asia remains the dominant growth engine, driven by industrial expansion, urbanization, and a growing need for reliable power generation. China and India, in particular, continue to pull significant LNG volumes into the market.

Europe, meanwhile, has reshaped its gas strategy rather than reducing its need. With pipeline supply constraints still in place, LNG imports have become a permanent fixture in the region’s energy mix. At the same time, new LNG-importing nations are entering the market, adding incremental demand that tightens the global balance further. Gas has cemented its role as a functional necessity—not just a transitional fuel, but a stabilizer in modern energy systems.

Supply: Still Playing Catch-Up

On the supply side, the response remains uneven. Years of underinvestment are still echoing through the system, limiting how quickly production can scale. While major exporters are expanding LNG capacity, these projects move on long timelines, meaning relief arrives gradually—not all at once.

Operational constraints add another layer of pressure. Maintenance cycles, unexpected outages, and infrastructure limitations continue to disrupt flows at critical moments. Even where production exists, the ability to liquefy, transport, and regasify gas efficiently is not always aligned. The result is a supply picture that feels constantly one step behind demand.

LNG Now Sets the Tone

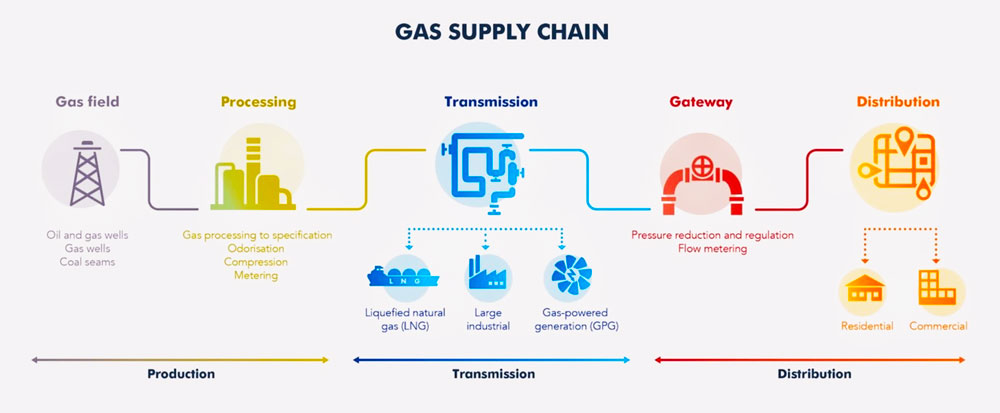

Liquefied natural gas has become the market’s central balancing force, effectively linking regional markets into a single global system. Cargoes now move fluidly toward the highest bidder, creating a competitive dynamic that keeps markets sensitive and reactive.

Europe and Asia remain locked in competition for available supply, particularly during peak demand seasons. Prices in the spot market can shift quickly based on weather patterns, storage levels, or disruptions in key export regions. At the same time, bottlenecks in shipping capacity and import infrastructure—especially in newer markets—are adding friction to an already tight system. LNG is no longer supplemental; it is the mechanism holding the market together.

Pricing a Market With No Cushion

Prices today reflect a market that understands its own constraints. While no longer at extreme highs, gas remains elevated compared to historical norms, and forward markets continue to signal tight conditions ahead. There is little indication of a near-term surplus.

Seasonality still plays a decisive role. Cold winters and hot summers can quickly push demand higher, tightening supply in short bursts. Storage offers temporary relief, but it is increasingly dependent on consistent LNG inflows to remain effective. In this environment, pricing is less about balance—and more about managing scarcity.

The Energy Transition Paradox

The shift toward cleaner energy is reshaping gas markets in complex ways. Investment in new fossil fuel supply has slowed, limiting future production growth. Yet at the same time, the intermittency of renewables has made gas more important as a flexible backup for power systems.

This creates a paradox: gas is being phased out in long-term narratives but relied upon heavily in real-world energy systems. The result is cautious investment, constrained supply growth, and continued demand support. Policy direction remains a key variable, but for now, gas sits firmly in the middle of the transition—not on the sidelines.

Where the Pressure Builds

The market’s tightness is unlikely to ease quickly, and several factors will determine how it evolves:

- The pace at which new LNG capacity comes online

- Demand acceleration in Asia and emerging economies

- Weather-driven consumption spikes

- Infrastructure expansion in importing regions

- Policy signals shaping long-term investment

MarketMind Insight

Global gas markets have shifted into a structurally constrained phase where imbalance is the baseline, not the exception. Demand is broad, resilient, and still growing, while supply remains slow to scale and operationally fragile. LNG has globalized the market, amplifying both competition and volatility. Until new supply meaningfully outpaces demand—and infrastructure catches up—tight conditions will persist, keeping gas firmly at the center of the global energy conversation.